by Richard C. Cook

featured writer

Dandelion Salad

February 3, 2009

A Bailout for the People:

Dividend Economics and the Basic Income Guarantee

By Richard C. Cook

Prepared for a Presentation at the

8th Congress of the U.S. Basic Income Guarantee Network and

2009 Eastern Economics Association Annual Conference

Sheraton New York Hotel and Towers

New York, N.Y., February 27

The existing monetary system is not free enterprise, and it is not capitalism. It is cancer.

Isn’t it Finally Time to Enact a Basic Income Guarantee?

The lack of individual and family income security in the midst of a highly-developed economy is a travesty under any circumstances. But the contradiction of “poverty in the midst of plenty” that has plagued the world since the start of the Industrial Revolution is becoming much more grave in the U.S. and abroad as the recession of 2008-9 worsens.

The problem does not lie with the production of goods and services which technology can accomplish abundantly. The problem lies with the distribution side of the equation. What people increasingly lack today is the money to purchase the necessities of life. Both the workplace and capital are idled because employees and consumers lack the purchasing power to buy the products and services our economy is capable of producing. The basic problem is excess capacity relative to available income.

Winston Churchill gave eloquent testimony to this conundrum of the modern age when delivering the Romanes Lecture at Oxford University on June 19, 1930. This was a few months after the crash of the U.S. stock market marked the start of the Great Depression. Churchill said:

“Who would have thought that it would be easier to produce by toil and skill all the most necessary or desirable commodities than it is to find consumers for them? Who would have thought that cheap and abundant supplies of all the basic commodities would find the science and civilization of the world unable to utilize them? Have all our triumphs of research and organization bequeathed us only a new punishment: the Curse of Plenty? Are we really to believe that no better adjustment can be made between supply and demand? Yet the fact remains that every attempt has failed. Many various attempts have been made, from the extremes of Communism in Russia to the extremes of Capitalism in the United States. They include every form of fiscal policy and currency policy. But all have failed, and we have advanced little further in this quest than in barbaric times. Surely it is this mysterious crack and fissure at the basis of all our arrangements and apparatus upon which the keenest minds throughout the world should be concentrated.

Evidently we’ve learned little since Churchill spoke. Isn’t it shameful—or just surprising—that since the proponents of “post-modern” economics restructured the U.S. economy around the concept of a deregulated financial sector over the past 30 years, income and wealth disparities between rich and poor have become much worse? Thus the ability of even middle-class people to pay for such basic needs as housing, food, medical care, and transportation falls ever further behind.

Perhaps we are finally ready to reopen the question of whether human beings have the right to an income sufficient to keep body and soul together even during difficult times. Within the U.S., this question has been mostly lost since President Ronald Reagan declared in his 1981 inaugural address that, “Government is not the solution to the problem; government is the problem.”

For it is only government that can authorize and implement what is called a Basic Income Guarantee (BIG). But if government is trapped in the ideological straightjacket Reagan and his fellow conservatives put it in, then the only possible outcome is Social Darwinism—i.e., survival of the fittest. We shouldn’t sugar-coat the pill. Social Darwinism is a death sentence for those unable or unwilling to claw their way to the top. Obviously voters repudiated this philosophy by the election of Barack Obama as president of the U.S. last November. Therefore the debate over implementation of a BIG that was abandoned over a generation ago should now also be reopened.

BIG Reconsidered

It is not difficult to see that implementation of a Basic Income Guarantee, had it been put in place when the concept still had political life in the U.S. during the 1960s and early 1970s, would have gone a long way toward ameliorating human distress from poverty along with assuring a significant degree of economic justice. And the population as a whole would clearly be much better off today, when loss of a job usually creates a family financial calamity, often with cancellation of health insurance and the risk of home foreclosure.

The last serious efforts at a BIG were President Richard Nixon’s Family Assistance Plan, which passed the House but was defeated in the Senate in 1970, and implementation of the Earned Income Tax Credit for low-income families, enacted in 1975 and extended by President Bill Clinton in the 1990s. Since the 1970s, almost every step toward economic “reform” has been one permutation or another of trickle-down economics, including the supply-side tax cuts of the Reagan and Bush II administrations.

Of course, the move to deregulate the financial industry that has been going on for three decades, along with the tax cuts for the upper brackets that characterized the supply-side approach, were supposed to have created a new “ownership” society based on having our money “work for us.” But the bubble economy that resulted from deregulation has now blown up, exposed as the biggest financial fraud in history. It is true that many more people now participate in the financial markets through mutual funds and 401(k) plans, but the value of these portfolios is ravaged during financial downturns like the one today.

Yet even in the midst of massive government bailouts for the banks and the as-yet-to-be-implemented economic stimulus proposals for the people, a BIG is never mentioned, not even by progressives. One problem with BIG is that its proponents often presented it as a transfer-of-wealth program, where a portion of the earnings of people with earned incomes would be diverted through taxation to support those in need. Even the idea of reducing military expenditures to support a BIG could be viewed as a transfer program, since a smaller war machine would mean a reduction of salary and benefit payments to military personnel and civilian contractors.

At times, some of those in favor of BIG have seemed to view it almost as a kind of charity. Others have pointed to a stronger moral grounding based on the fact that it is the whole of society that provides the vital ingredients for enterprises to be successful.

Bill Gates, for instance, could never have earned billions on his own. He depended on complementary industries, such as semiconductors, as well as an educated workforce, competent consumers, a strong patent and legal system, the transportation and retail infrastructure, etc. If it was society that provided such things, then society has a legitimate claim to sharing the proceeds based on its contributions.

One way the larger social contribution is acknowledged is through government’s claim on sharing the profits of enterprise through taxation. But taxation also is a burden that adds to the cost of products. Viewed simply as an additional cost, it is likely safe to say that a BIG has little, if any, chance to be implemented within the U.S. at any time in the foreseeable future, at least in an amount that would have an impact. In time of recession in particular, no one has the political appetite to argue in favor of a more equitable distribution of a dramatically shrinking economic pie.

But there are other ways to look at the problem. One is that of the Social Credit movement, where a regular dividend payment to individuals is seen not only as fair but is viewed as a necessary balancing force within a developed economy. A dividend in this case refers to a payment to all members of society based on the productive potential of the economy, not on tax revenues or government borrowing. But Social Credit concepts, while a force in the British Commonwealth nations, is virtually unknown in the U.S. Closer to home is the Alaska Permanent Fund (APF), where residents enjoy by right a share of the resource wealth of the state.

Both Social Credit and the APF as models for action will be discussed in this paper. The paper focuses on the U.S., though the concepts are applicable worldwide, and proposes a method of providing a BIG as part of a program to rebuild the economy from the bottom up. I call this program, based on dividend-type approaches, a “Bailout for the People,” as opposed to the bank bailouts that are adding trillions of dollars to the national debt and failing to revitalize the economy. I have presented this program previously in articles on the internet as “The Cook Plan.” (See “How to Save the U.S. Economy,” Global Research, October 10, 2008)

A Historic Collapse

As the recession deepens, with precipitous declines in employment, business activity, home appraisals, consumer confidence, and retail sales, it is evident that the U.S. and the world could be facing the possibility of an economic collapse of Great Depression severity. Officialdom denies it, but they also denied the recession was here until almost a year after the fact. Meanwhile, violent crime, stress-caused illness, and tension among nations are increasing.

Amazingly, it took a full year of economic distress, from December 2007, when economic activity last peaked, to a conference call on November 28, 2008, before the Business Cycle Dating Committee of the National Bureau of Economic Research declared that a recession had actually been taking place. As late as September 15, 2008, Republican presidential candidate John McCain said, “the fundamentals of our economy are strong,” a statement that mirrored what President George W. Bush had been intoning ever since the housing bubble began its rapid deflation in 2006.

But even with the economists and politicians finally acknowledging reality—it was the recession that propelled Barack Obama to victory—the situation is actually worse than they say. If economic health is measured, for instance, by immediate consumer purchasing power, it is telling that M1—the money in cash and checking accounts—has been decreasing, when adjusted for inflation, since December 2003. That was five years ago!

The decrease began soon after the Federal Reserve started raising interest rates following three years of cuts—over 500 basis points—that created the housing bubble in the first place. The bubble was the method chosen by the Bush administration and Federal Reserve to act as an economic engine after the recession of 2000-2001. Naturally, when they stopped inflating the bubble, cash-on-hand began to decline.

The recession is now settling in. The official unemployment rate was 7.2 percent at the end of December 2008, with half a million jobs disappearing per month. Major corporations in the retail, heavy equipment, and technology sectors—like Home Depot, Caterpillar, and Sprint—are shedding jobs by the thousands. So are the financial institutions that had grown so much they produced over $500 billion in profits as late as 2006.

Some commentators are predicting an unemployment rate of more than 10 percent within the next couple of months. Additionally, the number of underemployed or no longer seeking jobs is likely running at rate similar to the number officially out-of-work. According to John Williams’ Shadowstats website, unemployment including “discouraged workers” is almost 18 percent. Thus total unemployment could soon top 20 percent—close to Great Depression crisis conditions. Mere unemployment benefits cannot keep pace with this type of emergency.

Hence the action of the Obama administration to implement a major economic stimulus package. But will such a stimulus make a big enough difference? Can it be implemented in time? According to a January 26, 2009, report of the Congressional Budget Office, two-thirds of the proposed measures would be in place by September 2010, producing a “noticeable impact on economic growth and employment.” “Noticeable impact?” Is that good enough for a national and international crisis?

The fiscal reality is such that the federal government is poorly equipped to step in. The George W. Bush administration long ago reversed the Clinton budget surpluses by cutting taxes for the rich and through the enormous costs of the Afghanistan and Iraq wars.

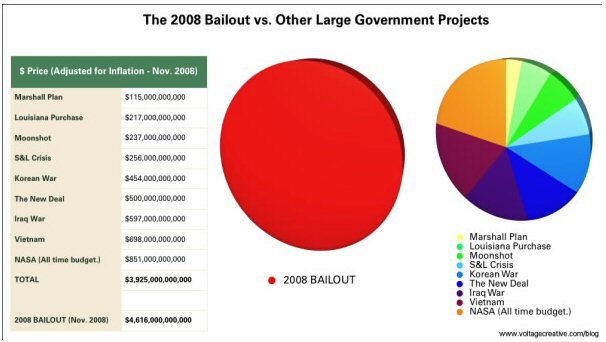

The federal budget deficit was added to significantly during the last six months of the Bush administration by former Secretary of the Treasury Paulson’s $700 billion financial industry bailout, along with other loans and bailouts to rescue Fannie Mae and Freddie Mac, insurance giant AIG, and additional emergency loans to banks and businesses from the Federal Reserve under Chairman Ben Bernanke. No one really has a handle on how much government money has been committed. $4+ trillion is a reasonable guess, though some estimates go as high as $8.3 trillion. The size of the bailout compared to government spending for major projects in history is shown in detail in the following graphic by www.voltagecreative.com/blog.

Still to come are any loans Congress or the Treasury will end up authorizing to save the auto industry and the costs of President Obama’s economic stimulus package that may approach $1 trillion. More bank bailouts may also be needed. According to Jonathan Macey of Yale University, author of a book about a bailout of Sweden’s banking system during the 1990s, “The pace of …bank losses is outrunning the infusions by the government.” Projections of more financial industry bailouts have been made by Vice President Joe Biden and House Speaker Nancy Pelosi. Fannie Mae and Freddie Mac may need an additional $16 billion.

During the coming two to three years the ratio of the national debt to GDP, which peaked at 125% in 1945, will likely exceed that record amount. The value of such a calculation is that it is transparent to inflation and may conveniently be compared to individuals in the same financial straits. What would happen to a family that each year incurred new debt at a rate of 125% of what they earned?

The difference between now and 1945 is that at the end of World War II American consumers enjoyed a high rate of savings due to full employment during the war, combined with a dearth of available consumer goods. After the war, these savings became available for the economic growth that paid down the national debt and created the boom of the 1950s. Today, consumer savings are virtually non-existent. And there is no assurance that more government spending will achieve anything like the full employment of the World War II era.

So the nation in 2009 is in uncharted territory, a scenario that is being repeated around the world with increased poverty, the decline of economic growth even in explosive economies like those of China and India, and imposition of more government austerities on less-developed nations by the International Monetary Fund. Again, under such circumstances, a Basic Income Guarantee, were anyone to consider it here or elsewhere, cannot be a simple transfer program, where those still with money are required to share a significant portion of it with those without. Rather new methods of funding must be found.

The Failure of Economics

So what is really wrong with the economy? Some say the housing bubble is the culprit, where the banks made credit so easy to acquire that the prices of homes inflated beyond their real value. Others point to the “toxic debt” from subprime mortgages that investment banks packaged and sold to unwary investors in tranches of mortgage-backed securities. Others blame the unregulated U.S. financial system which generated huge amounts of speculative investments, accomplished through bank leveraging, that now have gone sour. Here’s what economist Joseph Stiglitz wrote recently in Vanity Fair:

“Of course, the current problems with our financial system are not solely the result of bad lending. The banks have made mega-bets with one another through complicated instruments such as derivatives, credit-default swaps, and so forth. With these, one party pays another if certain events happen—for instance, if Bear Stearns goes bankrupt, or if the dollar soars. These instruments were originally created to help manage risk, but they can also be used to gamble. Thus, if you felt confident that the dollar was going to fall, you could make a big bet accordingly, and if the dollar indeed fell, your profits would soar. The problem is that, with this complicated intertwining of bets of great magnitude, no one could be sure of the financial position of anyone else—or even of one’s own position. Not surprisingly, the credit markets froze.”

Stiglitz is a former World Bank chief economist, a Nobel Prize winner, and professor at Columbia University. What is puzzling is his apparent lack of recognition of the role of collapsing consumer purchasing power as a cause of the freezing of the markets.

The following chart from www.Heritage.org compares growth in productivity to median household income within the U.S. over almost 40 years:

It is not difficult to see that individuals can no longer get loans because of the simple fact that they can’t afford to repay them. Businesses can’t get loans because declining consumer income is insufficient to buy their products. Within the U.S., consumer purchasing power has fallen not only because of the outsourcing of so many manufacturing jobs to low-paying overseas labor markets like China, but also because workers have not shared in the benefits of rising productivity.

As stated, for commentators like Stiglitz, or like Paul Krugman, another Nobel Prize winner who teaches at Princeton and writes for the New York Times, the debt-based monetary system run by the banks is a “given” as the unchallenged centerpiece of the world economy. But every debt a bank originates has to be paid, sooner or later, and paid with interest. The day of reckoning can be put off for a while by fresh lending, but not forever. If debt chronically outpaces earnings, the system will collapse.

Here is Krugman’s prescription from a November 18, 2008, column:

“What the world needs right now is a rescue operation. The global credit system is in a state of paralysis, and a global slump is building momentum as I write this. Reform of the weaknesses that made this crisis possible is essential, but it can wait a little while. First, we need to deal with the clear and present danger. To do this, policymakers around the world need to do two things: get credit flowing again and prop up spending.”

But even as Krugman and others argue for more government spending to prime the economic pump and restore employment—another trillion dollars added to the national debt can’t hurt, they say—such spending can only take place through more Treasury borrowing funneled through the Federal Reserve System. So their answer to a crisis marked by overwhelming public and private debt is more debt. This is where over-reliance on Keynesian economics has led. As Richard Nixon famously said back in 1971, “We are all Keynesians now.” It’s still the case in 2009.

The problem is that the world has changed radically since John Maynard Keynes wrote in the 1930s at a time when the banking system had discredited itself with the economic collapse that started the Great Depression. Then, the banks were contracting the currency and causing a liquidity shortage. But they were brought to heel by the federal government under President Franklin D. Roosevelt. To get things moving again, the government ran its own low-cost credit programs through agencies like the Reconstruction Finance Corporation. And while the government borrowed for job-creation programs like the WPA and CCC, business and household debt weren’t even close to what they are today.

What has happened since then is that the full-employment industrial state that was brought into existence in the U.S. by the New Deal and World War II, and which produced so much wealth that a BIG—then defined as a negative income tax—actually was taken seriously as a matter of discussion in the 1960s, no longer exists. Instead of the industrial state, we have what should be called the international “Empire of Usury.”

Road to Disaster

By the late 1960s the U.S. industrial state was being replaced by global outsourcing of manufacturing overseen by the financiers at the head of the largest American banks. Export of manufacturing operations to cheaper labor markets served a dual purpose: costs were reduced and payment of U.S. taxes by corporations could be avoided. A key event took place in 1971 when President Nixon removed the gold peg from the dollar and world currencies began to float. From that point on, credit became separated from production, and people began to look more to paper profits through currency, resource, and asset speculation as the source of wealth.

From 1971 onward, the financial magnates, located mainly in the U.S. and Britain, regularly made greater profits in currency trading and capital gains from asset inflation than in the production of goods and services. Who needed workers any more? Plus the U.S. was able to assure that the dollar would become the permanent world reserve currency by making it the standard for petroleum sales.

During the early 1970s, once removal of the gold peg made the quantity of dollars infinitely expandable, the U.S. government actively encouraged OPEC to implement radical increases in petroleum prices. The flood of “petrodollars” which resulted were deposited by the oil producers in U.S. banks or used to buy Treasury bonds. This money financed the growing U.S. trade and fiscal deficits and caused a sharp rise in inflation due in part to a devalued American currency. When the Federal Reserve under Chairman Paul Volcker began to attack the inflation with interest rates that would exceed 20 percent, the worst recession since the Great Depression followed.

This recession lasted from 1979-83 and wrecked the U.S. industrial economy. Never before in U.S. history had the financiers wielded such dictatorial—and destructive—power. The focal point of this power was David Rockefeller’s Chase Manhattan Bank. The revolving door between Chase and the U.S. government is illustrated by Volcker’s career.

Volcker began in 1952 as a Federal Reserve economist after being educated at Yale, Harvard, and the London School of Economics. He joined Chase as a financial economist in 1957. In 1962 he left for the U.S. Treasury Department and served as director of financial analysis. His boss was Rockefeller protégé Douglas Dillon, President John F. Kennedy’s Secretary of the Treasury. In 1963 Volcker became deputy under-secretary for monetary affairs.

In 1965 he returned to Chase as vice president and director of planning before heading back to Treasury in 1969 to spearhead the removal of gold convertibility. While still at Treasury, he became a founding member of David Rockefeller’s Trilateral Commission.

Then in 1975 Volcker became president of the Federal Reserve Bank of New York and was appointed to the Fed chairmanship in 1979 by President Jimmy Carter. Today Volcker is 81 years old. Now this quintessential Rockefeller technocrat is back as an adviser to President Barack Obama and head of the President’s Economic Recovery Advisory Board.

The last straw in the destruction of the U.S. as an industrialized democracy came when the financial industry began to be deregulated during the late 1970s to take advantage of the orgy of greed that had been made possible by government monetary policy. The bankers and multinationals didn’t care, because much of the U.S. trade deficit resulted from corporations buying from their own overseas subsidiaries whose products were then sold to American consumers on credit.

Accordingly, every period of domestic economic growth since then has been a financial bubble, including the merger-acquisition bubble of the Reagan/Bush I years, the dot.com bubble of the 1990s while Bill Clinton was president, and the housing/equity/derivative bubble of the 2000s during the George W. Bush administration. Each bubble was initiated by Federal Reserve interest rates cuts. Each was financed by massive bank lending, combined with foreign investment in the securities markets and tangible assets like real estate.

Every president since Reagan made his own contributions to the madness of financial deregulation. Meanwhile, the loss of manufacturing jobs that had started in the late 1960s and accelerated during the Volcker recession continued under President Bill Clinton, who signed NAFTA and gave China most-favored-nation status. The number of manufacturing jobs declined further under President George W. Bush.

Another feature of the bubble economy, especially during the 2000s, has been that growth, such as it was, has been tied to real estate through waves of construction for vast suburban tracts of new homes, retail mega-stores, upscale urban shopping/apartment/condo complexes, and gigantic new office buildings spread across the landscape as far as the eye could see. Industrial areas of former years were either converted to these uses or abandoned.

The retail stores are owned by the gigantic global conglomerates, sell mainly goods produced in China and other cheap labor markets, and employ low-paid domestic and immigrant workers. Managing it all has been a cadre of super-competent professionals and technicians, while the middle and skilled working classes of past decades have largely been replaced by computers. Among the few job categories that have grown significantly have been food service, health care, and law enforcement.

Home, store, and office construction have been financed not only through foreign capital, but also through huge bank loans capitalized by deposits from businesses which utilize overnight “cash management” accounts, by individual and institutional retirement savings, and by often-substantial federal, state, and local government cash reserves. The building booms pump money into the economy through the construction industry, and the accompanying price inflation results in capital gains that yield personal income and tax revenues. All of it is dependent on automobile transportation and increasingly-expensive gasoline. Not surprisingly, the oil industry, led by giants such as Rockefeller-dominated Exxon-Mobil, has been fabulously profitable.

But this spending—it really shouldn’t be called “investment”—does not lead to permanent prosperity. The cash flow stops when bank lending becomes over-extended and foreign capital dries up. In a downturn like today’s, price deflation of houses and stock markets destroys wealth that existed only on paper, eliminates income from capital gains, causes retail stores to shut down, erodes tax revenues, leaves office space empty, and strikes the construction industry and its spin-offs with loss of jobs. Unemployment in other sectors follows.

Most economists cling to the myth that what we have today is really free-market economics and fail to recognize the tremendous sea changes that have made the U.S. economy dysfunctional to its roots. This means that none of the standard solutions, which are aimed merely at re-inflating the bubbles, can solve the problem.

The stalemate is exacerbated by the fact that the era of worldwide U.S. dollar hegemony that has been in place since the 1970s has run head-on into the growing strength of a united Europe, a resurgent Russia, and the Asian economic powerhouses of China and India. These nations have caught onto the game the American banks have been playing. Removal of the gold peg by the U.S. in 1971 was the start of almost 40 years of monetary warfare against the rest of the world, which is finally saying “enough.” Unfortunately, with the U.S. consumer growing poorer by the day, fewer goods can be imported from other nations which suffer as well as their export-oriented manufacturing economies decline.

Let me also observe, with respect to the tender concern which economists have that the credit markets get up and running again, doesn’t this also illustrate the human tendency to “kiss the whip that scourges”? For the financial system holds everyone hostage, including citizens, politicians, and economists. An analogy might be the “Stockholm Syndrome,” where, as described by Yahoo.com:

“Captives begin to identify with their captors initially as a defensive mechanism, out of fear of violence. Small acts of kindness by the captor are magnified, since finding perspective in a hostage situation is by definition impossible. Rescue attempts are also seen as a threat, since it’s likely the captive would be injured during such attempts.”

The U.S. financial industry, which is the source of the disease, still is officially regarded by the federal government as “critical infrastructure”—i.e., sacrosanct—where anything that would threaten its dominance is seen as tantamount to terrorism or treason.

Cancer

The internationally-based Empire of Usury we have been watching collapse is a qualitatively different phenomenon from earlier phases of American history. It has little to do with any of the concepts we are so familiar with such as “democracy,” “business cycles,” or even “capitalism.”

In standard economic theory, capital is one of three necessary ingredients—along with land and labor—in the process of production. Utilization of each has a cost which is calculated in a myriad of ways. The technical term for this cost is “rent.”

The appropriate type of rent to be charged for the use of capital has been controversial down through the ages. Interest and dividends are two such types. What distinguishes today’s conditions is that control of capital is monopolistic, excessive, and entirely under the control of a parasitic sector, the financial industry.

An apt concept might be one drawn from medicine, since what we are seeing appears to be a rapidly metastasizing case of possibly terminal cancer. The host of this cancer is the economy of the U.S., and the cancer is deadly. The prescriptions of people like Stiglitz and Krugman, and even those now being presented President Barack Obama, are like offering a pair of crutches to a cancer patient so ill he can no longer even stand up.

The Empire of Usury is worldwide in reach and has a long pedigree. It goes back to ancient Sumeria, when debtors first began to be sold into slavery. Excessive debt ruined many of the Greek city-states and helped wreck the Roman Empire. During the Middle Ages, usury was viewed as such an evil practice that the Catholic Church outlawed it.

The current phase of the Empire dates to the creation of the Bank of England, which was a privately-owned banking institution that made its money by lending to the British government so it could fight its imperialistic wars. The Bank of England was cloned on American soil when the Federal Reserve System was created by Congress in 1913. The bankers had previously tried take control of the U.S. through the First and Second Banks of the United States but had been defeated by democratic forces led initially by President Thomas Jefferson (pres. 1801-09) and later Presidents Andrew Jackson (1829-37) and Martin Van Buren (1837-41).

Since the founding of the nation, there has been a struggle within the U.S. between pro-and anti-bank forces. Van Buren in his famous Inquiry into the Origin and Course of Political Parties in the United States (publ. 1867) traces the two-party system to this antagonism.

After a dramatic see-saw battle lasting two centuries, the banks finally saw complete triumph in the 1970s when the philosophy of monetarism took over and assured that a chronic insufficiency of real money in the economy would be answered by an exponentially growing amount of bank-generated debt. The flood of petrodollars overseas was paradoxically mirrored in reverse by a growing shortage of consumer purchasing power at home.

Monetarism was not directed solely by figures within the U.S. Rather it was part of a worldwide financier conspiracy. The “Reagan Revolution” which facilitated it was matched by “Thatcherism” in the U.K. and similar pro-bank regimes around the world. This included Australia and New Zealand, whose post-Great Depression prosperity was ultimately ruined by the new bank-centered financial policies.

Since American economists have failed so egregiously, we are forced to turn elsewhere for explanations. The triumph of usury—i.e., cancer—was ably described by New Zealand author Les Hunter in his 2002 book, Courage to Change: A Case for Monetary Reform.

“It was the artificial scarcity of money imposed by the application of monetarist policies that caused the usurious system to mutate from the industrial and allowed the collection of usury in amounts greater than that forthcoming as industrial economic rent. What has come to be practiced is a corruption of the investment practices that, in the past, and particularly in the industrial systems, had driven civilization forward.

“As investment proceeds within a usurious system, debt securities are accumulated and valued by the holders as income-earning assets. Of course, unlike the industrial assets such as the powered machine, a debt security produces nothing that is real.

“However, monetary income received as interest from compounding debt does give claim on current output—wealth at the point of sale—as does any form of economic rent once it has been collected in a monetized economy. Within usurious society, the rich are made richer and the poor, poorer, for no justifiable reason.”

How did this come about? Hunter writes in terms similar to those I used previously:

In the late 1960s, an aberrant socio-economic phase emerged: the usurious state, in which the control over money, rather than the ownership of machinery, is the most important lever of economic and social power. Investment in debt, and the speculative buying and selling of paper assets, are the most significant means of accumulating personal wealth.

Hunter provides the following list of characteristics of usurious systems, features that are agonizingly familiar:

- “Crushing debt;

- “A widening gap between rich and poor;

- “Share markets subject to collapse;

- “Currency meltdowns;

- “Mounting social distress;

- “A pervading belief that the free market should be allowed free reign;

- “Banks driven by profit but holding tremendous power through their ability to create and extinguish the national currency, that is, money.”

Hunter’s analysis is light-years ahead of U.S. economists, who, even when playing the role of an “official” opposition, really only enable the international financial elite to continue their dominance unabated. Of course industrial society is at the mercy of this financial tyranny, because huge quantities of money are needed for a modern economy to function. Hunter continues:

“The accumulation of usurious debt—money-lenders’ assets—became possible because those in business have an absolute requirement for access to sufficient working funds to pay costs. (The payment of costs is the main means of generating the national income; investment makes up the difference.)

“The money needed as working funds is defined as M1, which is the sum of base-metal coin, notes, and cheque money. It is this money that is accepted as the national currency. In many nations, applying monetarist policy has given business’s working funds—as the ancillary factor of production—sufficient scarcity value that significant amounts of usury, as the relevant form of economic rent, can be, and are being, collected.”

This system is not free enterprise, and it is not capitalism. It is the cancer that is destroying the world.

Revolution

The bankers’ takeover of the world economy that gained a complete triumph in the 1970s cannot be undone by President Barack Obama’s economic stimulus program or any other progressive nostrum. Even the goal of creating millions of new jobs, should it succeed, is not likely to compensate in the long run for the enormous amount of debt the productive economy is carrying. But then again, Obama does not intend to overthrow the Empire of Usury. After all, a main source of campaign funds for the Democrats in 2008 was Wall Street bankers and financiers.

The amount of debt the economy is carrying is staggering. If we count individual, household, business, and government debt, that figure now exceeds $40 trillion, including the recent bailouts. What the General Accounting Office calls “unfunded liabilities” of the federal government, due to future costs of entitlement programs like Social Security and Medicare, adds another $60 trillion. These estimates don’t include outstanding debt for derivatives, most of it bank-leveraged, which, according to the Bank for International Settlements, may amount to $1.28 quadrillion worldwide.

Growth in debt through 2006—understated, compared to figures derived by independent analysts—is shown by the following chart based on Federal Reserve figures. Note that virtually all of the debt has been incurred since removal of the gold peg and that its growth is exponential.

The commentators who write for newspapers like the Washington Post or give advice to the Federal Reserve have come up with solutions like slashing Social Security and Medicare benefits, a prescription President Obama will likely follow, or selling more U.S. assets to creditor nations like China. But they are proposing solutions in the interest of the financiers, not the nation.

They refuse to propose the obvious, which is that the debt must be written off as soon as possible and the monetary system changed to prevent further debt from being accumulated. Nationalization of the banks is not the answer; it still would be a debt-based system where the banks would rule from within the government rather than outside.

Bailouts financed by the government must be repaid with interest by the taxpayers. But the taxpayers are already overburdened by debt. Because the bankers are so untrustworthy and motivated by self-interest, they must be removed from power. This requires a political revolution that may already have begun.

The attack on the bankers’ power must be broad, persistent, and far-reaching. Today they control the political process in the U.S. and around the world. Their power is guarded by the laws and regulations of the Western nations. They control international agencies such as the International Monetary Fund and the World Trade Organization. They also influence the Western military and intelligence machines, with NATO now being sworn to protect Western “neoliberalism,” which means the bankers’ Empire.

The one U.S. political figure who has called for revolution is Dr. Ron Paul, Republican candidate for the 2008 presidential nomination and author of legislation to abolish the Federal Reserve System. But Dr. Paul still favors a largely unregulated bank-based system, though one where inflation is controlled through a metallic-backed currency. But there has never been enough gold and silver in existence to provide backing for the massive liquidity needs of an industrial economy.

In the past few weeks Democratic Congressman Dennis Kucinich—also a former candidate for his party’s presidential nomination—has spoken on the House floor in favor of placing the Federal Reserve under the Treasury Department. Kucinich also favors the American Monetary Act proposed by the American Monetary Institute. (www.monetary.org)

The American Monetary Act became part of Kucinich’s platform during his 2008 congressional campaign after he had dropped out of the run for the presidency.

This plan would eliminate public debt for federal government expenditures by returning to a Greenback-type system of direct government purchasing like we had during and after the Civil War. Public expenditures would focus on the creation of infrastructure assets as the basis for the monetary system. The Act would eliminate fractional reserve banking by requiring the banks to borrow money they lent from the government.

These measures would address the errors made by all Western governments by which, according to Canadian professor of economics John H. Hotson, they have violated “four common sense rules regarding their fiscal and monetary policies.” Hotson was professor emeritus of economics at the University of Waterloo and executive director of the Committee on Monetary and Economic Reform (COMER), when he identified these rules in 1996 as:

“1. No sovereign government should ever, under any circumstances, give over democratic control of its money supply to bankers.

“2. No sovereign government should ever, under any circumstances, borrow any money from any private bank.

“3. No national, provincial, or local government should borrow foreign money to increase purchases abroad when there is excessive domestic unemployment.

“4. Governments, like businesses, should distinguish between ‘capital’ and ‘current’ expenditures, and when it is prudent to do so, finance capital improvements with money the government has created for itself.”

The violations would be corrected by the reforms contained in the American Monetary Act. This would go a long way toward returning banking to its proper role of providing working capital for the economy but would displace the banking system as the focal point of national economic and political dominance. But these reforms by themselves still would not meet the need for a direct infusion of purchasing power into the hands of individuals. Fortunately, the American Monetary Act also contains a dividend provision, a deeply meaningful concept that we will now explore.

Key Discovery of the 20th Century: Dividend Economics

Perhaps 20-30 percent of the people in the developed world are doing just fine financially. They are either professionals, technical experts who are indispensable in making the world economy function, former government employees on pensions, or a small minority who live off compound interest—i.e., the bankers and the rich. Most of this 20-30 percent, particularly the latter group, do not seem to have a great deal of compassion for the majority within their own nations and even less for the billions of less privileged people around the world.

For the remaining 70-80 percent who realize, with the recession now having arrived, that their livelihoods are on a slippery slope downward, possibly taking them toward personal and family catastrophe, they need only one thing—MONEY!

For many of these it would be nice to have a job, or a better job. But jobs are not the answer, even though any time a politician, economist, activist, or commentator offers an opinion on how to improve the economy they say MORE JOBS! For example, in a recent article in Rolling Stone dated January 14 and entitled “Back to What Obama Must Do,” Paul Krugman wrote, addressing the new president:

“…you have to be really bold in your job-creation plans. Basically, businesses and consumers are cutting way back on spending, leaving the economy with a huge shortfall in demand, which will lead to a huge fall in employment – unless you stop it. To stop it, however, you have to spend enough to fill the hole left by the private sector’s retrenchment.”

But the advocates for government job-creation programs as the focal point of recovery are wrong.

The way to generate income security is not to give someone a job. It is to put money—cash—in his pocket. If we began with this simple fact the economy would soon generate far more jobs than people could fill. Of course some of these jobs would be low-paying or even volunteer jobs, which would be acceptable provided that people still had enough to live on and had opportunities to earn more.

For the world economy to function and for there to be enough produced to support everyone at a decent standard of living, not everyone has to work. In fact too many workers get in each other’s way. This accounts for the paradox which progressives despise that when companies eliminate jobs their stock value often goes up, because it’s a step toward becoming more efficient and more profitable.

In 2007 the world GDP was enormous–$55 trillion. The population was 6.6 billion. Per capita that’s $8,300. It’s not a large sum, but in many countries the cost of living is far lower than in the developed nations of the West. For a family of four the amount is $33,200. The point is that the world economy is capable of producing enough for all.

The productivity of a modern industrial economy is phenomenal. It surpasses the wildest dreams of generations past. The problem today is not a shortage of goods and services. It is often too many goods and services. For instance, there is a worldwide glut of automobiles. The same goes for many other items such as clothing and electronics. This does not mean that threats like climate change or resource depletion should be ignored. The reason these are not being faced is that industry must work so hard to cut costs and keep prices down in the face of the shortage of consumer purchasing power.

So why do we need more jobs? Only because we are so cheap and poorly informed that we fail to realize that a cash payment to everyone, at least at a subsistence level, should be viewed as a dividend. It’s something everyone should receive as the benefit of our incredible producing economy. A Basic Income Guarantee should be treated as a HUMAN RIGHT.

But the situation does not require that someone else should be taxed in order for that dividend to be provided. A BIG does not have to be a transfer payment or a share-the-wealth scheme. Rather it should reflect an acknowledgment by the economic system that the universe is bountiful and abundant. Modern industry has tapped into that abundance.

Today the abundance is being stolen by the bankers and their debt-based monetary system. This is what must be taken back by on behalf of “We the People.” This can be done by payment of a BIG as a dividend. It would not be inflationary, because it would not result in “more money chasing the same amount of goods.” Rather it would replace money borrowed from the banks or would generate new production.

If you want to read the history of dividend-economics, study the worldwide Social Credit movement originated by British engineer C.H. Douglas in the 1920s and 30s. I am not going to repeat that history here. I have written about it in articles over the past two years, most of which can be found at www.GlobalResearch.ca. It’s one of the themes in my new book, We Hold These Truths: The Hope of Monetary Reform (Tendril Press, 2008). You can find a lot of information about Social Credit on the internet, including the website for the Michael Journal in Canada at www.michaeljournal.org.

One of the world’s leading experts on Social Credit is Wallace Klinck of Alberta, Canada, who provides the following commentary on the crisis:

“The base cause of our essential economic and social afflictions is…a fundamental and widening disparity between effective consumer income and financial prices—resulting essentially from a basic flaw in national financial cost accountancy involving a premature withdrawal of credit because of added allocated capital charges in consumer prices. The consequent widening deficiency of effective purchasing-power forces the consuming public increasingly into dependency upon debt.

“We are now witnessing the inevitable, entirely predictable, and devastating results of such folly (or more likely, high policy). Governments are forced to make a futile attempt to ameliorate this problem by assuming debt to compensate or accommodate the ballooning private debt. I am sure that the financial powers look on with almost puzzled amusement as we engage in a sterile debate about the evils of interest and usury when we obviously have no strategy to deal with the rapid expansion of debt upon which interest is demanded. We waste our energy on a misguided and sterile debate while ignoring the fact that the consumer is charged with capital depreciation but not credited with capital appreciation.

“In other words, we blindly forgo our inheritance for a mess of pottage. You only pay interest on debt—eliminate debt and you have effectively eliminated any tribute of interest or ‘usury.’ There should be no need for any overall national consumer debt at all—consumers in aggregate should always be provided sufficient income to purchase the entire final product of industry without resorting to borrowing. The physical cost of production has been provided in full when goods are completed, and the financial means to liquidate the financial costs of that production should be made fully available as each ‘cycle’ of production is completed.

“Whatever the costs to industry, including interest or service charges, the consumer should always be in a position to liquidate them with his or her financial income. Being increasingly inadequate under the orthodox system of financial accountancy, that consumer income must be supplemented from a source which originates outside the price-system and does not, therefore, create new financial costs through its issue. The mechanisms to achieve this condition recommended by Social Credit are the payment to all citizens of a National Dividend and to all retailers a compensatory payment in order to effect a falling price-level, i.e., a Compensated Price.

“When the expenditure of human labor is being rapidly replaced by other factors of production, as it is in a most spectacular manner, talk of there being ‘no free lunch’ is entirely irrational from the standpoint of reason, downright sacrilegious from a theological standpoint, absolutely disastrous from an economic and social perspective—and absurd from a philosophical aspect.”

Mr. Klinck is explaining why everyone doesn’t have to work all the time for us to enjoy a decent standard of living. People in the U.S. understood this in the 1950s, when a single breadwinner could support a family. Does anyone wonder why conditions have changed so much for the worse since then when GDP is so much higher? In a private message to me dated December 13, 2008, Mr. Klinck made the following observations on jobs vs. income:

“I find it quite maddening that we have these recent desperate appeals for industrial state ‘bailouts’ to help industry go on producing even more unsalable goods, when it should be quite obvious that what needs ‘subsidizing’ is consumption and not production. Of course, as we know from a Social Credit perspective, these appeals are based on a number of major misconceptions about national cost accounting, the purpose of industry, work, and life in general. I think that this erroneous and indelibly entrenched ‘moral’ mindset is our biggest obstacle. For instance, I heard extended appeals on television today from the Canadian Autoworker’s Union for protection of their ‘jobs’, etc. If only we could show them that it is their incomes and not their ‘jobs’ which should be preserved. They are so obsessed with ‘work’ that they are blinded to reality.”

It’s a revolutionary thing to say, but it’s true. Unemployment does not have to be “bad” at all. It means fewer people have to work to make what society needs to function. It’s an indicator of greater efficiency. It’s only bad if jobs are the only way to provide people with income. Dividend economics shows that there are other, often better, ways.

Lessons from the Alaska Permanent Fund

We can find one small but extremely important example of dividend economics in the U.S. by examining the Alaska Permanent Fund, which paid every resident of Alaska a dividend of $3,269 in 2008 out of state resource revenues. The APF was set up in 1976 when Alaska voters passed a constitutional amendment calling for a direct payment to individuals rather than turning the money over to the state bureaucracy for “social services.”

Today the Alaska Permanent Fund is a shining—and rare—example of economic democracy at work. At first the APF made dividends incremental based on a person’s years of residency, but the U.S. Supreme Court declared this provision unconstitutional. The Alaska legislature responded by providing equal dividends to all residents of six-months or more. The first dividend, amounting to $1,000, was paid on June 14, 1982.

The APF dividend is not a welfare payment. It is a resident’s fair share of the bounty of the earth. There are no means tests, no lines to wait in, and no bureaucrats snooping around to find out what someone used the money for. The APF has not ruined the character of those who get it. A millionaire receives the same payment as a person living in poverty. Spent into circulation, the money becomes part of the lifeblood of the community without having to be repaid and with no interest being charged. Deposited into banks, the money capitalizes consumer borrowing and economic growth.

In the Fall 2008 Newsletter of the U.S. Basic Income Guarantee Network there appeared an editorial on the Alaska Permanent Fund by Karl Widerquist, one of the leaders of the worldwide BIG movement, now a professor at Reading University in England. This editorial is reprinted as follows:

“EDITORIAL: The Alaska Dividend and the Presidential Election (The views expressed in this editorial are my own and do not represent the views of USBIG or its membership. -Karl Widerquist)

“Most people will be surprised to learn that the Republican vice-presidential nominee and the Democratic presidential nominee have both endorsed the Basic Income Guarantee. In one form or another both support policies to guarantee a small government-provided income for everyone. As reported in the USBIG Newsletter earlier this year, Obama has voiced support for reducing carbon emissions with the cap-and-dividend strategy, which includes a small BIG.

“Sarah Palin, like most Alaskan politicians, supports the Alaska Permanent Fund. Existing rules caused the APF dividend to reach a new high of 2,069 this year. That much had nothing to do with Palin. But, whatever else you might think of her, she deserves credit for adding $1200 more to this year’s dividend.… She proposed it to the legislature, and pushed it through, resisting counter proposals to reduce the supplement to $1000 or $250.

“Most people who learned about Palin at the Republican National Convention in August would probably be surprised to learn that such a hard-line conservative supports handing out $16,345 checks to even the poorest families. Actually, families the size of Palin’s will receive $19,416—no conditions imposed besides residency, no judgments made.

“The support of politicians like Palin provides evidence against the belief that BIG is some kind of leftist utopian fantasy with no political viability. In the one place BIG exists it is one of the most popular government programs, and it is endorsed by people across the political spectrum.

“The APF has not become an issue in the campaign, and I doubt she has plans to introduce a similar plan at the national level, but when the issue has come up, Palin has taken credit for it as a conservative policy. In an interview on the Fox News network, Sean Hannity confirmed that Palin increased the Alaska dividend by $1200 this year. Hannity commented, ‘I have to move to Alaska. New York taxes are killing me.’

“Sounding like some kind of progressive-era land reformer, Palin replied, ‘What we’re doing up there is returning a share of resource development dollars back to the people who own the resources. And our constitution up there mandates that as you develop resources it’s to be for the maximum benefit of the people, not the corporations, not the government, but the people of Alaska.’

“Tim Graham, writing for the conservative website Newsbuster.com criticized NPR’s Terry Gross for asking questions that implied opposition to the APF in an interview with Alaska Public Broadcasting host, Michael Carey. Graham writes, ‘Gross walked Carey through the idea that it’s not hard for Palin to be popular in Alaska when she’s handing every family a $1200 check from all the oil business. She then elbowed Carey about how that money could have been better “invested” (as Obama would say) in government programs.’ Suddenly conservatives are ridiculing people they assume do not support unconditional grants.

“Palin justified a tax increase on the oil companies to support higher BIG on the PBS Now program before she was nominated for vice-president. ‘This is a big darn deal for Alaska. That non-renewable resource, of course, is so valuable …. And of course [the oil companies] they’re fighting us every step of the way when we say, “Well we wanna make sure, especially as it’s being sold for a premium, that we’re receiving appropriate value.” … The oil companies don’t own the resources. They have leases and the right to develop our resources for us. And we share a value, we’re partners there, because they do the producing for us. But we own the resources.’ …

“The lesson here is that the APF is a model ready for export. Readers of this newsletter will know that governments in places as diverse as Alberta, Brazil, Iraq, Libya, and Mongolia have recently thought seriously about imitating the Alaska model.

“Some might be tempted to think that the APF isn’t a true BIG and it isn’t motivated to help the poor. Not so: Jay Hammond, the Republican governor of Alaska who created the APF, came all the way to Washington, D.C., to speak at the U.S. Basic Income Guarantee Network conference in 2004. He told me that his intention was to create a BIG to help everyone—most especially the disadvantaged. If he had his way the APF fund would now be producing dividends four to eight times the current individual level of $2,069.

“Others might dismiss the Alaska model saying that it is a unique case because Alaska has so much oil wealth. Again, not so: Alaska ranks only sixth in U.S. states in terms of per capita GDP, with an average income just over $43,000 in 2006, more than $15,000 per year less than number-one Delaware, and only $6,000 per year ahead of the national average. Any other state or the federal government can afford to do what Alaska has done.

“Alaska has oil wealth; other states have mining, fishing, hydroelectric, or real estate wealth. Governments give away resources to corporations all the time. The U.S. government recently gave away a large chunk of the broadcast spectrum to HDTV broadcasters at no charge. Offshore oil drilling will soon be expanded on three coasts. Everyone who emits green house gases and other pollutants into the atmosphere takes something we all value and—so far—pays nothing.

“What was different about the Alaskan situation was that Jay Hammond was there to take advantage of the opportunity. With the Alaska model in place, it will be just a little easier for next person at the next opportunity.”

There have been other times in U.S. history when the government “gave away” wealth. An example was the Homestead Act of 1862 which opened the American heartland to settlement and helped create one of the world’s most productive agricultural regions. There was also a time when anyone who walked into a U.S. Mint could have their gold or silver stamped into coinage—a critical financial service offered to the public free of charge. Land grants to the railroads also helped capitalize the growth of that industry.

So why isn’t a dividend like the one provided through the Alaska Permanent Fund paid to every U.S. resident or, for that matter, to every person in the world? Please don’t make up any phony “economic” answers to this question. The answer is obvious—everyone else is being cheated by the monetary system.

The “Cook Plan”

What I am calling the “Cook Plan” would be an effective way to implement dividend economics. The plan is to pay each resident of the U.S. a dividend, at first by means of vouchers for the necessities of life, in the amount of $1,000 per month per capita starting immediately. It would be our fair share of the resources of the earth and the productivity of the modern industrial economy. Under the plan, the money would then be concentrated through deposit in a new network of community savings banks to capitalize lending for consumers, small businesses, and family farming.

I am calling it the “Cook Plan” because I have been advocating such measures for almost two years, every since I published my first article on the subject in April 2007 entitled: “An Emergency Program of Monetary Reform for the United States.” (See Global Research at http://www.globalresearch.ca/index.php?context=va&aid=5494) One reader who has responded favorably to the plan calls it “Trickle-Up Economics.”

Because we are talking about a dividend, there would be no means test. Everyone—rich, poor, and in-between—is entitled. The dividend would total about $3.6 trillion, which, not by coincidence, is the amount of new debt U.S. residents must incur each year from banks simply to exist. That borrowing, of course, is on top of borrowing in past years, because most people do not entirely pay off old loans before taking out new ones. Debt in this country in recent years has been cumulative, with interest constantly compounding. The annual dividend I have proposed would bring a halt to this “Grip of Death,” as it has been termed by British author Michael Rowbotham in his book: The Grip of Death: A Study of Modern Money, Debt Slavery, and Destructive Economics.

Because we have all been brainwashed to believe that the only possible sources of government funding are through taxes, user fees, or the national debt, it is difficult to believe that a dividend of $3.6 trillion could be paid to residents by other means. In fact it could, and it would not even require a fund to be set up like the Alaska Permanent Fund that is replenished by resource revenues such as oil leases. According to Social Credit theory, the dividend fund could be created sui generis; i.e., it could be created out of “nothing.”

And why not? John Maynard Keynes pointed out, and everyone realizes today, that the banking system does just this in creating money “out of thin air.” It’s what many people refer to as “printing money,” which the Federal Reserve is doing on a massive scale in bailing out the financial system.

The banks that belong to the Federal Reserve use the purchase of Treasury debt as collateral, but the money itself is issued as credit as a multiple of the reserve base. The trouble is we end up paying interest on it, which is why the interest on the national debt in the fiscal year 2009 budget totals more than $500 billion. (Of course one reason adding to the federal deficit today looks so attractive as a means of recovery is that the interest Treasury has to pay is so low—but it is still borrowing.)

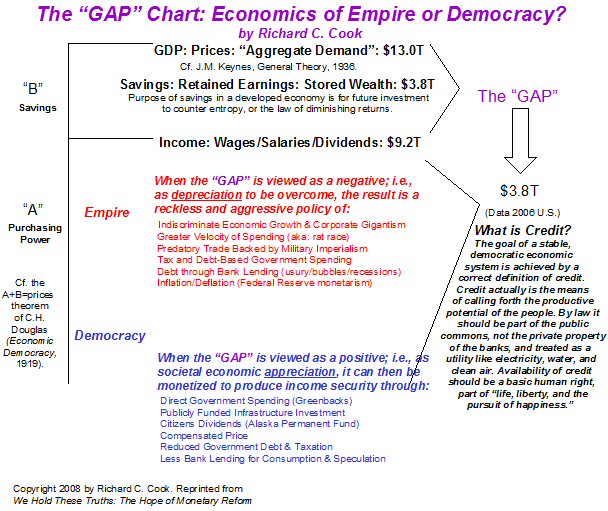

Issuance of credit is mis-defined today as the private property of the banks. I point this out in the “GAP Chart” in my book We Hold These Truths: The Hope of Monetary Reform. I state in the chart:

“The goal of a stable, democratic economic system is achieved by a correct definition of credit. Credit actually is the means of calling forth the productive potential of the people. By law it should be part of the public commons, not the private property of the banks, and treated as a utility like electricity, water, and clean air. Availability of credit should be a basic human right, part of ‘life, liberty, and the pursuit of happiness.’”

Today the banking system has a monopoly on credit which it has seized unlawfully from the government, where, under the U.S. Constitution, Congress alone, according to Article II, has the prerogative to, “coin money and regulate the value thereof.” There is no reason except bankers’ propaganda why the federal government, as authorized by Congress, could not issue credit through a citizens’ dividend, by direct government spending, or by other means such as loan guarantees or grants/loans for infrastructure. This would be real economic democracy.

The “GAP” Chart is presented in its entirety as follows. What the model shows how we can monetize the productive potential of the nation that today is held back by businesses from payout as wages, salaries, and dividends through the withholding of retained earnings. It is these retained earnings that the business will utilize later to renew its processes of production through investment. But while these funds are idle, their creative potential still exists. That potential is the “energy source” for new consumer purchasing power. It is real, though, like electricity, invisible until harnessed.

As I explain in We Hold These Truths: The Hope of Monetary Reform:

“In order for people to be able to pay for a nation’s GDP, sufficient purchasing power must be generated. Purchasing power is what British economist John Maynard Keynes called ‘aggregate demand.’ But the income that is generated through wages, salaries, and dividends is never enough to consume the GDP, because a portion must be withheld (saved) as retained earnings for future investment. This is the ‘gap.’ The way society decides to fill the gap reflects whether it views itself as an empire, where the rich profit at the expense of the many, or a democracy, where all members of society have the opportunity to prosper. Under the imperial design, the ‘gap’ is viewed negatively and filled by bank lending at usurious rates of interest, foreign conquest, the economic growth imperative, aggressive trade policies, or inflation of the currency. But when, by contrast, the ‘gap’ is viewed as an opportunity to further democratic ideals, it can be monetized through public control of credit and issued as direct government spending, a citizens’ dividend, or low-cost credit. This monetization of savings reflects a definition of credit as a public utility, not the private property of the banks. Keynesian economics tries to compromise between the imperial and democratic ideals by using government debt to monetize savings, but this ultimately destroys the currency through bankruptcy or inflation. Today we are at a late stage of imperialistic monetary policies which have led to financial collapse. Democratic management of credit has been tried at various times in U.S. history with great success [e.g., through the Greenbacks] but never on a sufficient scale to transform the economy. It is now time to take decisive measures to replace the economics of empire with those of democracy.”

Under the “Cook Plan,” the U.S. Treasury would issue the dividend against an account that represents the productive potential of the nation once the money is spent. As stated earlier, the dividend would not be inflationary, because it would replaced money borrowed from banks for consumption and would be matched by the production of new goods and services within the physical economy.

In fact a dividend would have far less tendency to inflate than do Federal Reserve Notes, because it would not have bank interest charges added to it which ended up in prices charged consumers at the point-of-sale. And once created the dividend would remain in circulation—or deposited as savings—because it would not have to go back to a bank to be canceled as loans now do.

Savings would also be an important part of the plan, because today citizens have completely lost the ability to save in the usury-based economy where cancellation of bank credit along with the interest charged sucks up all available cash from people’s pockets. And the dividend would not be taxed.

The dividend would be issued as vouchers as a temporary measure until the program caught on and it was clear the money would be spent responsibly. The vouchers would be redeemable at any location licensed to do business for necessities of life such as food, housing, transportation, clothing, communications, or business/home maintenance. In fact they could be used for most purchases except things like the lottery, alcohol, entertainment, etc.

Once received in transactions, providers would then deposit the vouchers in the community savings bank that had been set up in their locality. In order to maintain membership in the bank, providers would be required to keep a certain amount of money on deposit to capitalize lending by the bank within the community. Loans would be made available under the bank’s fractional reserve privileges and would be issued at low rates of interest, preferably no more than one percent plus a premium for default insurance, depending on the credit status of the borrower. Persons eligible for lending would include individuals, householders, students, small businesses, local manufacturing concerns, family farmers, etc.

It should be obvious that this system would completely transform and revitalize local economies in any nation where it were implemented. One of the worst features of today’s usury-based economy takes place when global companies in league with the banks come into communities and destroy local businesses by underpricing them. Then these companies extract all the liquidity from the community, where people usually are so cash-poor they buy mainly with credit cards, and return only a fraction to the low-wage workers they employ.

The “Cook Plan,” with the direct injection of purchasing power into the community through vouchers, combined with a new system of low-cost credit, would transform this dire situation completely. It would allow people to live and prosper without dependence on credit cards, government job-creation programs, or government welfare bureaucracies. And it would allow a resurgence of volunteer activities and work at lower-paying professions such as family farming, education, and the arts.

In fairness to Paul Krugman, he does propose spending not tied to employment as well as tax cuts. In his Rolling Stone open letter to President Obama he states that:

“…aid to the distressed – enhanced unemployment insurance, food stamps, health-insurance subsidies – is both the fair thing to do and a desirable part of your short-term economic plan.”

This is not far from advocating a Basic Income Guarantee, except that, once again, Krugman would fund such spending from federal borrowing. But he is leaning in the right direction. A little further and he will arrive at the “Cook Plan,” which would have a much better chance of fulfilling President Obama’s campaign slogan of rebuilding the economy “from the bottom up” than what is the essentially top-down government-directed program his administration is now proposing.

What amount would the stimulus add up to? The “Cook Plan” would result in $3.6 trillion the first year of implementation being directly added to consumer income, or about 25 percent of the GDP. Debts could be repaid, money could be saved, the necessities of life would be assured, and a renaissance in local, rural, and regional economies would come about within a few years.

Finally we would have the “leisure dividend” the industrial age promised but never delivered. And we would have resolved the “Curse of Plenty” cited in the quotation from Winston Churchill at the start of this paper. These objectives would be achieved not through the chimera of government-engineered “full employment”; i.e., socialism, but through income security leading to real economic freedom and democracy.

The proposal encapsulates the essence of dividend economics by acknowledging the right of the individual to obtain a significant measure of economic freedom through the fact of membership in a society that is heir to the genius of past generations in creating the material environment in which we live.

This heritage is not the property of the banks, and it is not the property of the government. It is the property of the people. The conservative model of government exemplified by the ideology of today’s Republican Party subjects people to a bank-run collectivism. And even the most benign progressive model exemplified by ideology of the Democratic Party still subjects us to the collectivism of tax-borrow-and-spend job-creation programs that may or may not work.

So let a national system of dividend economics now be implemented, a plan that draws on much of the wisdom that has been dormant in recent decades as the Empire of Usury has suffocated the life out of the world’s economy. It is now time to put that wisdom to work. “We the People” deserve to live in freedom on this beautiful planet, no matter what the bankers say. In fact such a program would be a major step upward in human social evolution.

Do It Now

Obviously it would take time—though not much time—to work out all the details of the program. But in principle, the “Cook Plan” is sound, with the total dividend being recalculated each year. Remember again that the dividend takes a power of nature and what should be a public utility—credit—and gives it back to the people as a human right rather than the private property of the banks. We cannot afford to wait. Conditions today are nearing an emergency. Thousands of people are losing their jobs every day as the recession turns into a monster.

Wallace Klinck sums it up

“If society had followed the Social Credit policy of C. H. Douglas who advocated Consumer Dividends and Compensated Retail Prices instead of the Fabian Socialist social debt policy of the late economist John Maynard Keynes, none of the current madness would have occurred. We would be enjoying increasing prosperity with falling prices and increasing leisure as should be the case in any modern and civilized society.”

Copyright 2009 by Richard C. Cook

Richard C. Cook is a former U.S. federal government analyst. His book on monetary reform, We Hold These Truths: The Hope of Monetary Reform,is now available at http://www.amazon.com. He is also the author of Challenger Revealed: An Insider’s Account of How the Reagan Administration Caused the Greatest Tragedy of the Space Age.

From the archives:

Credit As A Public Utility: The Solution to the Economic Crisis by Richard C. Cook (videos)

How to Save the U.S. Economy by Richard C. Cook

Richard Cook: “It’s Time to Fix the Monetary System” by Mike Whitney

Dennis Kucinich Takes An Hour To Explain Our Current Economic Situation

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Pingback: The Coming Revolution: Evolutionary Leap or Descent Into Chaos and Violence? | Dandelion Salad

Pingback: Peak Inequality: The .01% And The Impoverishment Of Society by David DeGraw + The Economics of Revolution | Dandelion Salad

Pingback: America the Betrayed by Richard C. Cook | Dandelion Salad

Pingback: Money for the People: Grillo’s Populist Plan for Italy by Ellen Brown | Dandelion Salad

Pingback: Richard C. Cook: Creating Local Currencies and Monetary Reform « Dandelion Salad

Pingback: Seeing Through the Illusion of Money by Richard C. Cook « Dandelion Salad

Pingback: Richard C. Cook goes straight to the heart of the matter by Jamie Walton « Dandelion Salad

Pingback: “Job Creation”–Stupid Is as Stupid Does by Richard C. Cook « Dandelion Salad

Fascination. I could not help but contemplate how the earliest visitors and brave settlers felt as they left their former lands, homes, families and started new without the burdens of a corporate church, oppressive monarchy, heavy tax burdens to meet a new way of life.

This new life of many new trails and errors but great freedoms. And now look at how the system they ran from has caught up with us due to greed and corruption and a learned (taught) acceptance of this distructive system.

Our present state and how we got here tells me a new plan is the only plan and the “COOK PLAN” may be the answer.

Pingback: The Historical Roots of the Economic Crisis – The Cure: Monetary Reform by Richard C. Cook « Dandelion Salad

Pingback: Corbett Report: Economics 101 with Richard C. Cook « Dandelion Salad

Pingback: Thomas Greco’s “The End of Money and the Future of Civilization”: A Review by Richard C. Cook « Dandelion Salad

Pingback: American Monetary Institute 2009 Conference: “We Shall Prevail” by Richard C. Cook « Dandelion Salad

Pingback: How to Finance the National Dividend? by Richard C. Cook « Dandelion Salad

Pingback: Faux “Progressives” By Timothy V. Gatto « Dandelion Salad

Pingback: Towards a sound economy By Rudo de Ruijter « Dandelion Salad

Pingback: The Report from Iron Mountain Revisited by Richard C. Cook « Dandelion Salad

Pingback: Urgency of the American Monetary Act by Richard C. Cook « Dandelion Salad

Pingback: A Meditation on Our Monetary System: State of Permanent Siege* By Richard Cook « Dandelion Salad

It’s gonna take a bit of a reread to follow this, especially the first part about monetism. But it’s insightful to put ‘dividend’ money into the hands of the people, provided they spend it wisely (even if it is monopoly money).

Not sure how this achieves the dismantling of the Fed and monetism and usury, but it’s a start: Bail out the People.

Provided, however you’d not end up with a bunch of fat, lazy Alaskans who kill things for fun with all their state-sponsored free time… It’s unfortunate that leisure seems not to beget enlightenment.

But it’s logical that people will then spend locally, and the economy will trickle-up. Part of the ‘restrictions’ on what you get to buy with this ‘dividend’ has to be no equities, no bonds, no investments, no gold, no hoarding, no off-shoring, and no spending at big-box stores or firms or suppliers that offshore supply and labor, and no polluting producers, and no firms receiving corporate welfare already like big ag. And no guns or ammo. And no slot machines. Nothing can be ‘off the books’.

You’d have to have an expiry on the vouchers, and a strict set of businesses you’re allowed to spend them on, who’d have to then be incentivized as ‘certified’ to keep commerce in the community, and be willing to subject themselves to massive regulation and oversight.

Then there’s the complication of the ‘welfare state’– while the ‘welfare queen’ is a fabrication of the free-marketeers, people do get lazy if you give them a thousand bucks a month to spend, and a whole lotta people will do just fine on that, in fact likely will find some way to spend it on drugs, or transfer them somehow off the books.